[ad_1]

Pay attention

to this Gas for Thought podcast.

Mainland China’s transition to electrification reached a serious

milestone in July 2024 when gross sales of new-energy automobiles (NEVs)

surpassed inner combustion engine (ICE) automobiles for the primary

time, in line with knowledge launched by the China Passenger Automobile

Affiliation (CPCA).

NEVs embody battery electrical automobiles (BEVs), plug-in hybrid

automobiles (PHEVs) and range-extended electrical automobiles (REEVs). In

2023, automakers’ aggressive gross sales promotions and a tidal wave of

new mannequin launches helped to spice up gross sales of NEVs in mainland China

after the 2022 withdrawal of the central-government subsidy

applications.

It’s past doubt that the Chinese language auto market will proceed to

transition to electrical automobiles within the subsequent few years with

automakers advancing their electrification plans. S&P World

Mobility expects that NEV share of the Chinese language passenger automobile

market will attain 46% in 2024, in comparison with 36% in 2023.

The acceleration available in the market’s shift to EVs will likely be helped by

declining battery costs, a wider availability of fashions and the

intense stage of competitors that exists available in the market.

With NEVs going mainstream, tendencies taking form within the sector

have begun to have an effect on the broader passenger automotive market and affect

client decisions.

EV adoption more and more pushed by plug-in hybrid

fashions with BEV gross sales slowing down

Though purchases of BEVs, PHEVs and REEVs are all eligible for

the central-government’s buy tax discount incentive applications

by means of 2027, what is absolutely accelerating the market’s shift to

electrification in 2024 are PHEVs and REEVs, reasonably than pure

electrical automobiles.

Within the first half of 2024, Chinese language gross sales of BEVs rose by 12%

12 months over 12 months to three.02 million items, by comparability, gross sales of

PHEVs, together with automobiles with extended-range electrical powertrain,

surged by 85% 12 months over 12 months to 1.92 million items within the first

half of this 12 months.

These market dynamics had been already taking form in 2023. S&P

World Mobility analysis reveals that mixed gross sales volumes of PHEVs

and REEVs within the passenger automobile market surged by 83% 12 months over

12 months in 2023 to 2.75 million items, whereas that of BEVs grew by 20%

to five.2 million items.

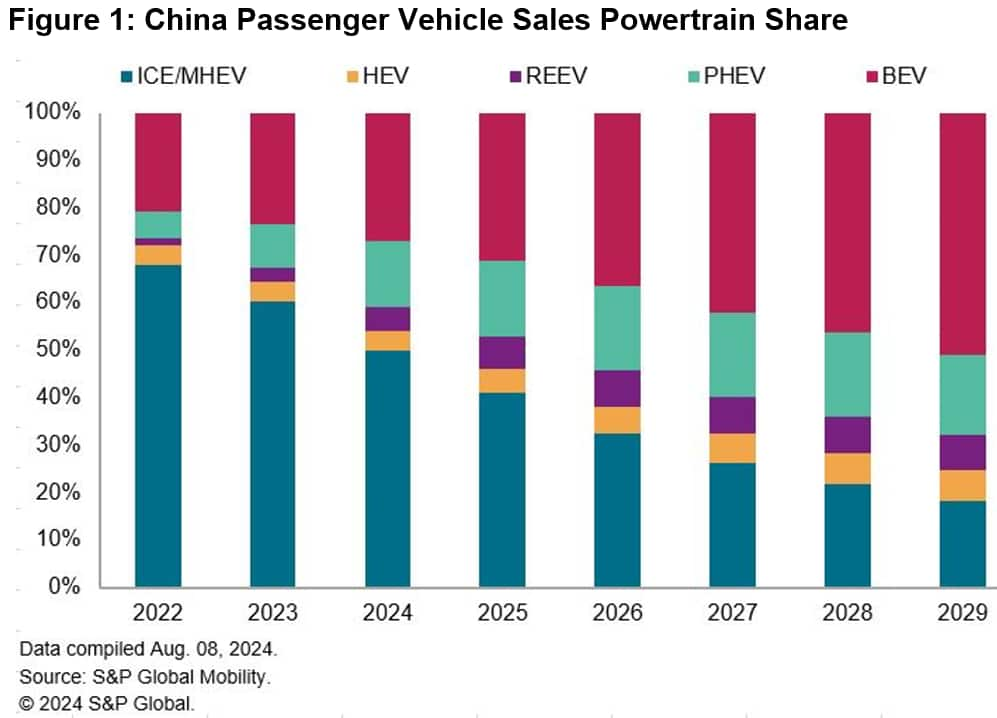

S&P World Mobility expects PHEV and REEV gross sales in mainland

China to proceed to develop within the subsequent few years, accounting for twenty-four%

of complete passenger automobile gross sales by 2029. Regardless of a slowdown within the

annual development fee, BEV gross sales share is predicted to succeed in 51% in

2029. Collectively, the entire NEV gross sales share can be 75% that 12 months,

in line with S&P World Mobility forecasts.

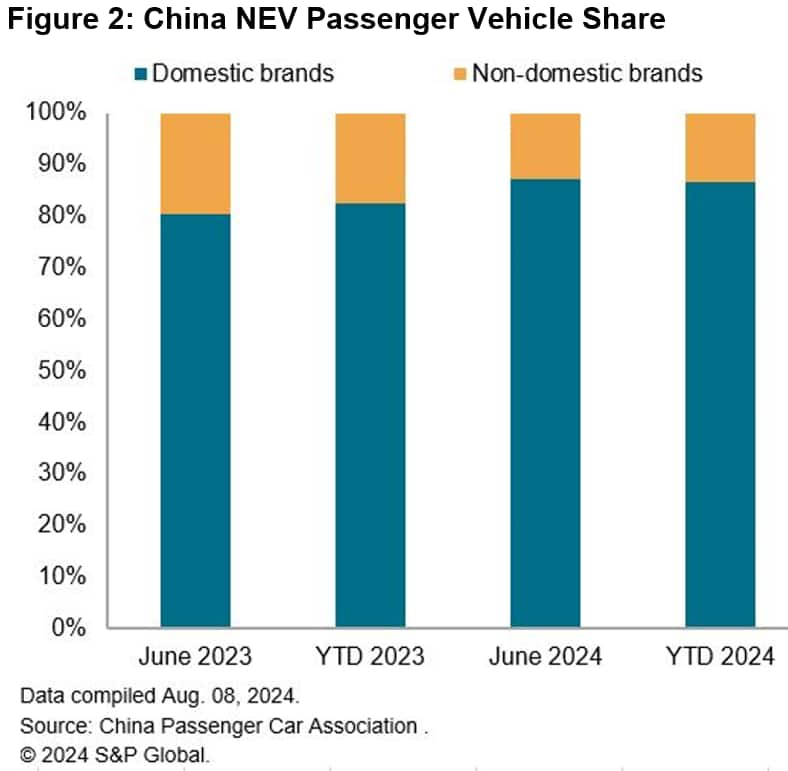

Chinese language manufacturers’ robust presence within the NEV market has helped

them to advance their market share within the total passenger automobile

market. Home manufacturers’ market share within the Chinese language retail

passenger NEV market elevated from 83% within the first half of 2023

to 87% within the first half of 2024, whereas their international counterparts

have a mixed gross sales share of lower than 15% within the first six

months of 2024.

Chinese language OEMs’ rising presence within the NEV market has led to a

shift in client preferences over manufacturers and fashions. World OEMs,

particularly the Japanese manufacturers, have struggled to match their

Chinese language rivals within the pace of adapting to altering client demand

and market circumstances. Toyota has already lower manufacturing at its

Chinese language JVs by 22% 12 months over 12 months within the first half of 2024 to manage

with declining demand. Nissan and Honda, the opposite two main

Japanese automakers in mainland China, have all recorded big

declines in Chinese language gross sales throughout 2024, confronted with BYD’s aggressive

product offensive.

As well as, the premium automakers, together with the massive 3 German

manufacturers, additionally face the problem of commanding a value premium for

their new-generation BEVs as value competitors intensifies. To maintain

up with the pace of innovation in China and cut back improvement

prices, VW is working with Xpeng and SAIC Motor on separate EV

applications that may use the 2 Chinese language firms’ automobile platforms

and software program applied sciences. VW’s upcoming new launches in mainland

China may even embody long-range PHEVs and REEVs developed

collectively with SAIC.

S&P World Mobility’s newest projection reveals Chinese language

manufacturers’ gross sales share within the nation’s passenger NEV market is about to

attain 87% in 2024, additional bettering from 83% in 2023. With international

automakers rolling out their new-generation BEVs and PHEVs in

mainland China within the subsequent few years, we count on international manufacturers’

market share to enhance from 2026 onwards to succeed in 25% in 2029 with

VW and BMW contributing strongly.

Chinese language tech firms tapping into client

preferences for SDVs

Software program is more and more a degree of distinction in influencing

shopping for alternative in mainland China. Rising client curiosity in

software-defined automobiles (SDVs) presents a chance for

mainland China’s tech firms to faucet into the electrical automobile

market.

Xiaomi Company, a number one good cellphone producer, goals to

ship 100,000 EVs this 12 months. The corporate’s first electrical mannequin,

the SU7 sedan, has obtained unprecedented publicity in mainland

China because of Xiaomi’s robust model enchantment, its big client

electronics merchandise userbase and new good automotive options it

launched to the SU7.

China’s telecom large Huawei additionally emerged as a serious participant in

the NEV sector, offering a spread of clever automobile

applied sciences to its OEM companions. The success of AITO, a

Huawei-backed NEV model, has inspired China’s state-backed

automakers together with BAIC and JAC to forge partnerships with Huawei

to transition their product line with software-defined automobiles.

China’s export surge met with new commerce

limitations

Though electrification in mainland China continues to develop,

the nation’s standing as an EV manufacturing and export hub could face

some challenges.

Mainland China’s EV exports surged previously two years amid

automakers’ efforts to broaden gross sales in international markets. Information from

the China Affiliation of Vehicle Producers (CAAM) suggests

China’s NEV exports reached 1.2 million items in 2023, in contrast

with lower than 680,000 items in 2022.

Though Tesla contributed largely to mainland China’s EV export

surge in recent times, rising EV cargo volumes of Chinese language

automakers together with SAIC and BYD has fueled issues over China’s

overcapacities and its intention to dominate the worldwide market with

low-price automobiles.

The EU’s provisional tariffs, which provides as much as 36.3% of customized

duties to Chinese language-built BEVs, are the newest instance of rising

protectionist actions taken by main economies to guard their

market from the inflow of BEVs originating in China. Canada and the

US have additionally introduced strict tariffs on China-made BEVs.

Automakers wish to deal with these commerce limitations by

shifting manufacturing of sure fashions to different manufacturing

areas or investing in native manufacturing capacities to bypass

tariffs. The excessive tariffs may even immediate automakers to additional

optimize their value construction to take care of an affordable margin

stage.

Nonetheless, throughout the automotive sector, main international automakers

together with Stellantis and Volkswagen are looking for their very own method to

sustain with competitors from Chinese language rivals. Each automakers have

invested in Chinese language EV startups previously 12 months to realize entry to

EV know-hows—particularly software program structure—and pace up

new launches. The Stellantis and Leapmotor three way partnership already

started cargo of Leapmotor EVs in-built mainland China to Europe

in July.

To deal with the EU tariffs, Stellantis additionally kicked off meeting

of the Leapmotor T03 EV at its plant in Poland from

semi-knocked-down kits imported from mainland China.

S&P World Mobility affords detailed sales-based

powertrain forecasts for the USA, Canada, Brazil, United

Kingdom, Italy, Germany, France, Spain, Netherlands, Sweden,

Norway, Remainder of EU30, India, mainland China, and Australia.

This text was printed by S&P World Mobility and never by S&P World Scores, which is a individually managed division of S&P World.

[ad_2]