Nearly all of the growing older inhabitants in Japan nonetheless prefers utilizing money for transactions, in keeping with a current report citing authorities information. In 2023, cashless transactions in Japan totaled 126.7 trillion yen ($885 billion), accounting for 39.3 p.c of all spending within the nation, stated the Japanese authorities. The federal government hopes that quantity reaches 40 p.c by 2025.

The Japanese authorities’s initiative to extend cashless transactions is being supported by a Tokyo-based startup referred to as SmartBank, which presents an app and companies that make switching to cashless funds simpler for folks.

Shota Horii (CEO of SmartBank), alongside along with his twin brother Yuta Horii (CTO) and Jun Taketani (CXO), based the corporate in 2019 after promoting their earlier firm, Fablic, to Rakuten in 2016. Whereas working Fablic, the three found that many customers have been nonetheless utilizing money for on a regular basis monetary transactions. The founders launched SmartBank in an effort to deal with an issue throughout the shopper finance business in Japan.

SmartBank’s main goal customers are people of their 20s and 30s searching for to handle private funds, in addition to married {couples} seeking to handle their funds. Now the corporate says it has greater than 1 million downloads, however they didn’t present the variety of customers.

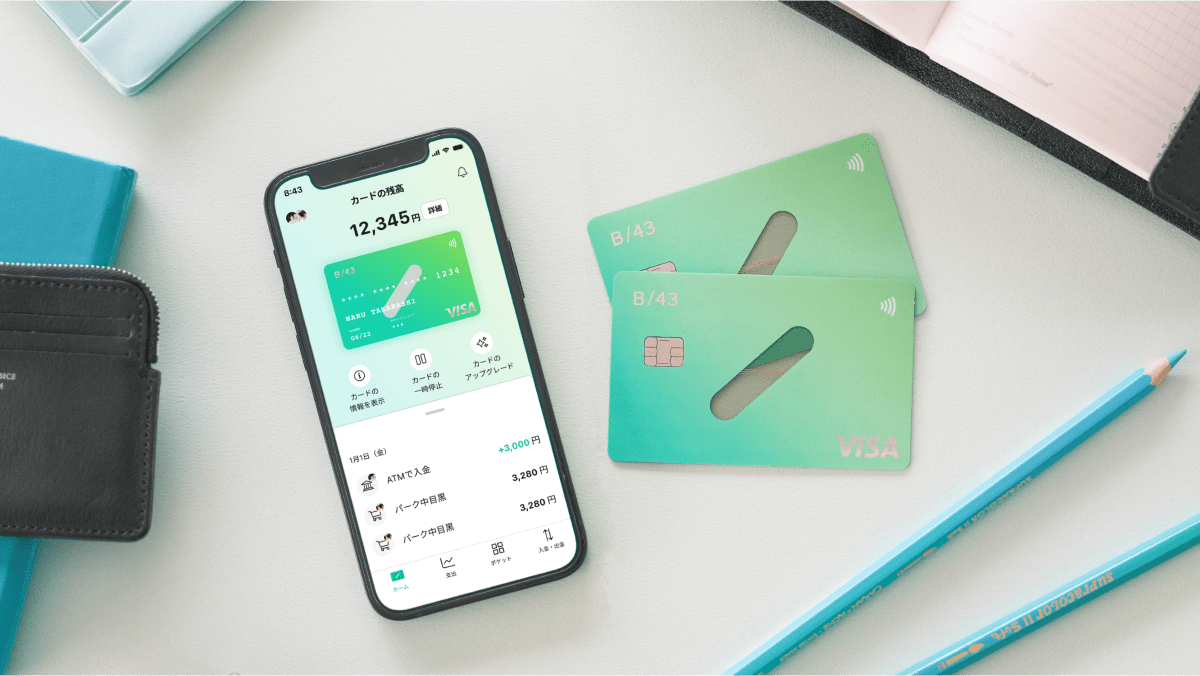

Its core product is a pay as you go card and a finance administration app that gives a deposit account. Its pay as you go playing cards embrace the B/43 My Card, the Visa-branded fee card for single people; the B/43 Pair Card for customers to handle their funds with their companions; and the B/43 Junior Card for teenagers.

“Our core consumer base,[which was B/43 My Card], is now the B/43 Pair Card customers…that is vital as banks in Japan don’t present joint financial institution accounts, and B/43 has grow to be the go-to product,” Shimogawara stated.

The startup stated Tuesday that it has raised 4 billion JPY ($26 million), with 1.1 billion JPY ($7.2 million) coming from debt financing and a couple of.9 billion JPY ($18.8 million) from fairness supplied by its present investor, World Mind. The fairness capital is from a fund fashioned with SMBC, one of many largest banks in Japan. As of April 2024, SmartBank had raised a complete of 5.93 billion JPY ($38.5M) in fairness and 1.1 billion JPY in debt since its inception. The startup will use the brand new capital to double down on hiring from 49 workers in October to round 100 staff by 2025; half of the entire workforce would be the engineering group, SmartBank CFO Yuta Shimogawara stated in an unique interview with TechCrunch.

The newest funding comes roughly two and a half years after its Collection A, $20M, in July 2022. The startup has since then expanded its consumer base and product choices with the purpose of turning into a complete monetary platform like a financial institution, offering a variety of economic companies to customers sooner or later.

Simply final month, the corporate launched an AI receipt studying characteristic by utilizing generative AI expertise to rework its app into an AI-driven monetary advisor, stated Chihaya Akaike, the director of enterprise operations at SmartBank. This characteristic helps customers higher perceive their funds, optimizes and automates monetary actions, and allows them to make use of, save, and make investments their cash, Akailke advised TechCrunch.

“Shopper fintech companies in Japan have been sluggish to make use of AI, however our purpose is to grow to be the main AI fintech firm within the nation,” Akailke continued.

On high of that, the corporate not too long ago added a characteristic permitting customers to attach their bank cards and financial institution accounts to B/43 to get a holistic view of their funds. “We shall be making our service accessible to non-card customers as we open it in order that customers can begin utilizing B/43 with out issuing a card and by merely linking their current bank cards and financial institution accounts, which will even develop our income stream,” Akailke defined.

SmartBank obtained a license for cash transfers three years in the past, permitting customers to withdraw their deposits in money. It additionally acquired a pay as you go fee instrument license in April, enabling the startup to carry customers’ deposits. The licenses assist the corporate supply companies like funds and P2P transfers.

Its friends like MoneyForward and Zaim can not maintain customers’ deposits, which limits their capability to help customers in managing their private belongings, resembling financial savings and investments, in keeping with the corporate.

The five-year-old outfit plans to diversify income streams past its interchange charges (IRF), the place most income comes from. Along with IRF, it has applied different companies like Purchase Now Pay Later (BNPL), subscription (B/43 Plus), and referrals, Akaike stated.

{kind=link}